Demolished buildings in the city of Homs (Reuters)

Demolished buildings in the city of Homs (Reuters)

Demolished buildings in the city of Homs (Reuters)

A

A

A

A

A

A

Enab Baladi – Jana al-Issa

Three out of six public banks in Syria provide real estate loans. However, although the terms and conditions set forth by the banks for real estate loan approvals are difficult to meet, the Syrian regime still promotes “their great benefits” in securing funds to stimulate the real estate market and boost the economy.”

In fact, real estate loans pose additional burdens on citizens amid rising real estate prices compared to the monthly income in Syria. This year, real estate prices have increased by nearly 100 percent.

In this article, Enab Baladi discusses considerations related to the feasibility of real estate loans granted by banks in Syria to find out who is benefiting from these loans and how they will contribute to the economy’s growth.

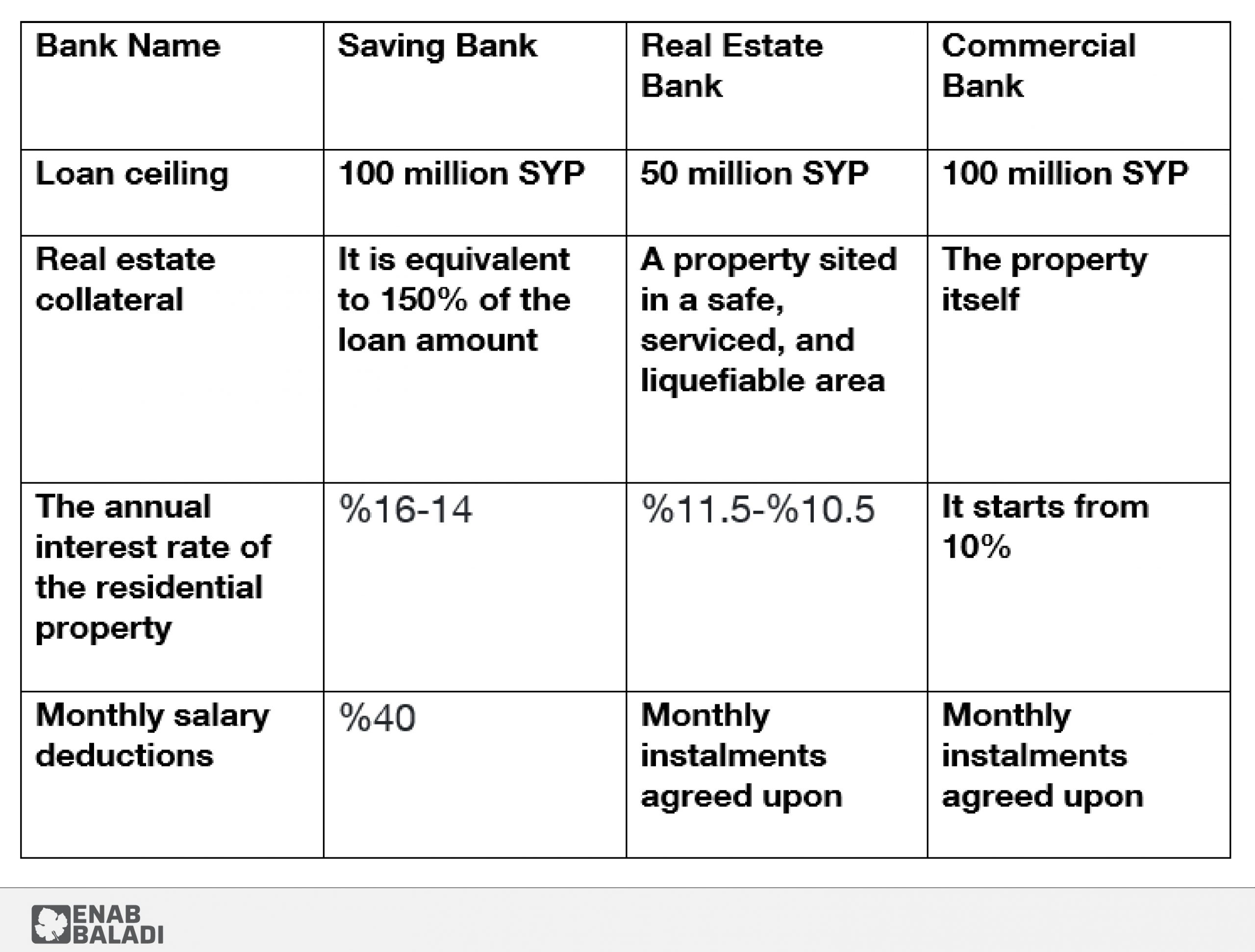

In September 2020, the Commercial Bank of Syria began granting real estate loans with a ceiling of 100 million Syrian Pounds(1USD=3,470SYP).

Then, the Real Estate Bank started to grant real estate loans last July, with a ceiling of 50 million SYP.

Finally, the Savings Bank began providing loans with a ceiling of 100 million SYP in early August.

While the eligibility criteria to get a loan varies based on the collateral put up by the borrower, whether cash, other securities, or a letter of credit, the Syrian state media continues bragging about real estate loans and their benefits for the Syrian economy and citizens alike.

When applying for a real estate loan, a guarantee is required. This guarantee means that the applicant for a loan must mortgage a property in his name until the loan is repaid.

Thus, a person who does not own property cannot apply for a real estate loan, except in the case of a commercial bank loan, in which the property itself serves as collateral for the loan.

Syrians—including only public and private sector workers, retirees, military, business owners, professionals, artisans with a commercial, industrial, professional or crafts record for not less than one year, and scientific professions affiliated with the union for at least one year—can obtain commercial real estate loans.

Real estate expert Ammar Youssef described the mortgage loan offered by Syrian banks as “unfeasible, not applicable, and ineffective in the market,” based on the lack of demand for such loans.

In an interview on 4 August, Youssef told the pro-government al-Watan newspaper that the aim of real estate loans is “the operationalization of deposits,and funds accumulated in banks.”

Firas Shabo, who holds a Ph.D. in financial and banking sciences, told Enab Baladi that the conditions associated with granting loans are never compatible with people with limited income.

Shabo considered that “the value of these loans cannot even buy you a property, as the absolute ceiling of such loans is 100 million SYP (approximately 33,000 USD). This explains why many people do not consider obtaining real estate loans.

Firas Shaabo does not believe that the loans offered can solve the housing problems today. Plus, real estate loans do not impact the real estate market; they cannot either revive the sluggish market or reduce property prices.

Firas Shaabo indicated that only a “very small group” of Syrian people could benefit from real estate loans.

Shaabo added this group must meet the eligibility criteria for obtaining a property loan; a person must be able to provide security of roughly 150 percent of the value of the loan amount.

The applicant must allocate 40 percent of his monthly income to pay off his existing loan. Ninety percent of Syrian people cannot afford this because they are below the poverty line, according to UN figures.

The majority of Syrians cannot afford to pay the interest due on real estate loans. The average real estate interest rate is typically 16 percent, a percentage that most Syrians cannot afford. Given the worsening economic situation, most Syrians have come to consider owning a property as a “luxury,” because they are already struggling to provide their families with food and other essentials, according to Firas Shaabo.

Shaabo indicated that only wealthy or financially secure people could benefit from the existing real estate loans. This segment of people is “very small.”

On the other hand, these loans constitute an extra burden on lower-income people, “who are not able to think of luxuries.”

The Syrian daily newspaper al-Baath, which speaks for the ruling Arab Socialist Baath Party, published a report on 17 August titled “In the Field of Credit and Loans… the weakest link was those with low incomes[…]. This report shows that banking products in their current forms target only specific groups. They may not yield any fruitful outcomes, mainly regarding the neediest group, whether individuals or micro-enterprises.

According to the report, current loans provided by banks contribute to widening the gap between the social classes. The report indicates only “financially secure people” can expand their activity at the expense of small projects exploited by large companies.

Dr. Firas Shaabo believes that the development of the mortgage credit system to include a more comprehensive proportion of citizens is directly related to the structure of the country’s economy.

Shaabo indicated that if there was a reviving economy capable of producing more goods and services, a currency whose value did not change much, and a state that provided essential services and infrastructure to the people and investors, the economy could potentially be revived.

The citizens of this hypothetical country would be able to obtain loans while having the ability to repay them simply because their country’s economic activities were recovered and revived.

Yet what is happening in Syria is the exact opposite, according to Firas Shaabo. The Syrian regime is constantly working to besiege citizens through banks; it deepens the “bad relationship” between them, created by the depreciation of the Syrian pound and the imposition of specified deposit amounts for set periods of time in exchange for various sales operations.

Firas Shaabo believes that there are no “promising” economic visions in the foreseeable future because of the absence of purchasing power and economic life. Furthermore, the state does not play its role as a primary supporter of service and social life.

No banking and financial policy can contribute to resolving the Syrian economic situation, according to Shaabo.

The real estate market in the areas under the control of the Syrian regime was characterized by a greater stagnation in the buying and selling activities than in previous years, an expert in engineering economics, Muhammad al-Jalali told al-Watan, a pro-government newspaper.

Al-Jalali explained that the main reason for the stagnation in the market is the fall in demand for real estate due to the high prices of real estate compared to income and the difficulty in the movement and transfer of funds.

Al-Jalali pointed out that if a person wants to buy a property for 200 million SYP, for example, he will have to transfer this amount through the banks. However, he will only be able to withdraw it in installments for a long time at a rate of only two million per day. “And this has negatively affected sales activities.”

The real estate market in regime-controlled areas is witnessing stagnation after the Syrian regime took measures and released many laws, including the real estate tax law, which depends on collecting the tax on properties sold based on their current value, rather than the approved value in the financial records.

Citizens refrained from buying real estate due to the depreciation of the Syrian pound against the US dollar and the difference between the exchange rates on the black market and the official rates set by the Central Bank of Syria.

if you think the article contain wrong information or you have additional details Send Correction

More Economic Reports

More Economic Reports